DRC Artisanal Diamonds Achieve Strong Results in Antwerp Auction

Artisanal diamonds from the Democratic Republic of Congo (DRC) have achieved a positive result in Antwerp, selling above expectations in a landmark auction designed to improve market access for small scale diamond producers.

The sale, organised by the Antwerp World Diamond Centre through its OrigemA programme, featured 103.77 carats of fully traceable rough diamonds sourced from artisanal mining cooperatives in the DRC.

The diamonds achieved an average price of $66 per carat, exceeding the estimated market value of $58 per carat. The total sale value reached approximately $6,000, demonstrating the potential for responsibly sourced artisanal diamonds to compete successfully in the international marketplace.

OrigemA was created through collaboration between Belgium and the DRC to connect artisanal miners with global diamond markets. The programme aims to ensure that more value from diamond production remains within local communities, supporting areas such as mining development, agriculture, healthcare and education.

Karen Rentmeesters highlighted that the auction demonstrated Antwerp’s continued role as a leading rough diamond trading centre, where international competition helps achieve fair market pricing.

The result also reflects a wider industry movement toward greater transparency, traceability and responsible sourcing as consumers increasingly seek confidence in the origins of natural diamonds.

Diamond Industry Adapts as Producer Countries Take a Greater Role

The natural diamond industry continues to adjust to changing consumer behaviour, economic uncertainty and evolving market conditions. However, industry leaders believe important foundations are being created for future growth.

World Federation of Diamond Bourses president Yoram Dvash noted that one of the most encouraging developments is the increasing participation of African producer nations across the diamond value chain.

Countries including Botswana and Angola have strengthened their involvement through their affiliation with the WFDB, while other producing nations such as Rwanda are also seeking a larger role in shaping the future of the diamond sector.

This reflects a broader shift where producer countries are looking beyond mining and becoming more involved in trading, manufacturing, marketing and value creation.

The potential future ownership changes surrounding De Beers, currently controlled by Anglo American, further highlight the changing structure of the global diamond industry.

Greater participation from producing countries could create stronger alignment between miners, manufacturers, traders and retailers, helping build a more balanced and sustainable diamond ecosystem.

Traceability and Consumer Confidence Become Industry Priorities

Transparency remains a major focus for the diamond sector as companies work to strengthen consumer trust.

The acquisition by Gemological Institute of America of a stake in De Beers’ Tracr platform represents continued movement toward verified diamond provenance and digital traceability.

As laboratory grown diamonds become more prominent in the market, the natural diamond industry is placing increasing emphasis on communicating the rarity, geological history and emotional value of natural diamonds.

Industry leaders continue to stress the importance of investment in marketing and education to help consumers understand the differences between natural and synthetic diamonds.

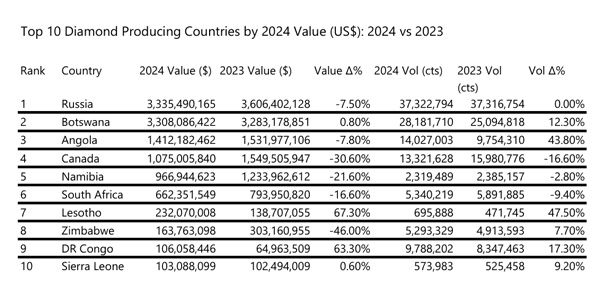

Russia Holds the Largest Share of Global Diamond Reserves

Global diamond supply remains concentrated among a small number of countries, with Russia holding the largest known reserves.

Russia accounts for almost half of the world’s diamond reserves, significantly ahead of Botswana, which holds approximately 250 million carats, representing around 14.7% of global reserves.

Other major reserve holders include Angola and the Democratic Republic of Congo, each with approximately 150 million carats, while South Africa holds around 87 million carats and Zimbabwe approximately 56 million carats.

Together, Russia and Botswana account for close to 60% of global diamond reserves, highlighting the concentration of future supply potential.

Africa continues to play a central role in the natural diamond industry, with Botswana, Angola, the DRC, South Africa and Zimbabwe collectively representing a significant share of known reserves.

The Future of Natural Diamonds

The diamond industry is entering a period of transformation. Greater producer involvement, improved traceability, responsible sourcing and renewed consumer education are reshaping the market.

While challenges remain, the continued focus on transparency and cooperation across the diamond pipeline provides a pathway toward a stronger future for natural diamonds.

The industry’s ability to adapt while preserving the rarity and uniqueness of natural diamonds will remain central to maintaining consumer confidence and long term value.

Source: DCLA