Nirav Modi fled India in 2018 to evade the law days before a case was registered against him and his associates.

By Press Trust of India: Gold, platinum, diamond and jewellery of Firestar Diamond International, owned by fugitive diamantaire Nirav Modi, will go under the hammer on March 25, according to a sale notice.

De Beers has increased prices of small rough diamonds for the second consecutive sight as a combination of demand and supply factors continue to create a hot market for the category.

Prices for tiny stones rose by around 10% on average at this week’s trading session, with sharper advances in certain segments, customers and insiders estimated Monday. The changes were mainly for minus-7 sieve sizes, which weigh about 0.03 carats, across a range of qualities. De Beers was unavailable for comment.

The February sale runs this week from Monday to Friday in Gaborone, Botswana.

Rough under 0.75 carats became a sought-after asset in the second half of 2022 as melee demand from luxury brands strengthened and Indian manufacturers needed cheaper material to fill factories amid thin profit margins. In addition, Western sanctions on Russian diamonds created a mixture of real and perceived shortages in those sizes, for which Alrosa is the biggest supplier. The trade is watching for potential further restrictions as the one-year anniversary of Russia’s invasion of Ukraine approaches.

“Are people preempting what the [new] measures might be on Russia? [The strong market] might have to do with that,” a rough-market participant told Rapaport News on condition of anonymity.

Last year, De Beers made only modest increases in the prices of smalls, even when the segment saw robust demand, a sightholder explained on condition of anonymity. The miner raised prices at last month’s sight by approximately 10% — alongside decreases in the slower, larger goods.

The fresh hikes caught many dealers by surprise, as they were expecting De Beers to monitor the Chinese recovery before making further price adjustments.

Group of Seven nations and the European Union are discussing ways to track Russian diamonds across borders, a move that could pave the way for restrictions on their trade in future, according to people familiar with the matter.

Previous EU attempts to sanction Russian gems have run into resistance from importer nations such as Belgium who argue that the effort would be futile because transactions will simply shift elsewhere without a mechanism to trace precious stones.

A diamond’s origin is clear at the start of the supply chain when it is issued a certificate under the Kimberley Process, which was designed to end the sale of so-called blood diamonds that financed wars. But after that they can become difficult to track.

Cut and polished stones are often intermingled at trading houses and the original certificate will be replaced with “mixed origin” documentation, making it near-impossible to keep track of where Russian diamonds are eventually sold.

The US has sanctioned the Russian mining giant, Alrosa PJSC, which accounts for about a third of the $80 billion global trade in rough diamonds. But the measures have had limited impact as much of the trade flows through other markets such as India.

The people with knowledge of the G-7 and EU discussions said a solution is not imminent, because tracing polished diamonds in a global market is extremely complicated. Still, two of the people said the G-7 could issue a statement on the matter as early as next week as part of the effort to maintain pressure on Russia as its war in Ukraine approaches the one-year mark.

It’s hard to believe that COVID first hit just over three years ago.

After the original shock that the pandemic caused, especially when lockdowns were put in place in large parts of the world in early 2020, markets, rather than continuing to crash, instead surged higher.

Stimulus programs from both central banks and central governments, which were enormous in scope, were the primary cause of this surge, with the vast quantity of dollars fed into the system leading to one of the biggest rallies in the share market, cryptocurrencies, and even real estate on record.

Since late 2021 it’s been tough going though, with the last twelve or so months particularly challenging for most investors.

Many seemingly don’t know what to do, with survey data suggesting many are stuck in terms of ideas, a subject we discuss below.

There are however always a select group of investors who do get ahead of the curve, recognise changing patterns for what they are, and act accordingly.

We think pink diamond investors fit that mould, and despite the current economic climate and investor hesitance, we’ve seen a continued appetite for pink diamonds first hand.

This is something we expect to see continue across the course of this year, as more and more investors seek exposure to this niche asset class, which has proved quite lucrative for many.

Investor uncertainty in challenging market

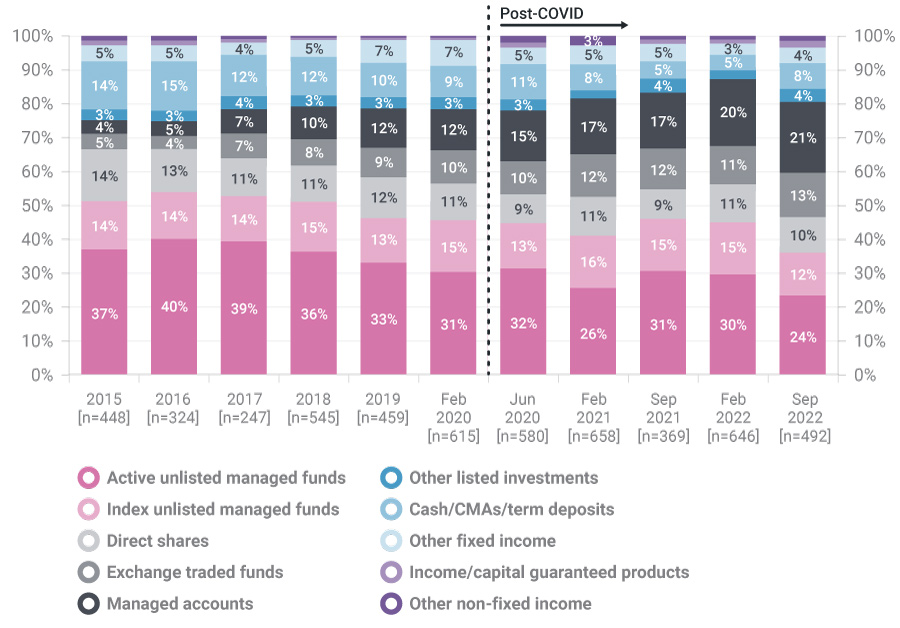

In early February, we read an interesting report containing six insights into the way Australians invested their money in 2022.

As we alluded to in the introduction to this week’s update, last year was very challenging for investors, with stock markets plunging quite rapidly at one point (on this note, while the Australian market fell, it fared better than most), cryptocurrencies falling by more than 50% in most cases, and even real estate turning south, with the Australian property market now on track to see its biggest decline in decades.

We also saw the return of inflation, which soared beyond 5%, and in some developed countries beyond 10%, in the fastest pace of consumer price rises seen in decades.

What did investors do in response?

Turns out much of the same, with the following chart showing that despite a few tweaks, they kept investing money in pretty much the same way they always have.

Trend: Allocation of new client inflows

In the last year, roughly what proportion of the new client inflows you advised on went into each category? Averages among financial advisers.

The only notable change looking at this, and other data in the article was an influx of money into fixed income and cash ETFs, presumably due to the higher interest rates that started to flow through across 2022.

While that’s understandable, given rising inflation, those cash and fixed income assets also lost value last year, failing to act as a safe haven in any meaningful way.

The only investors that thrived last year were those who looked through the conventional wisdom on how to invest (i.e. keep nearly all your money in stocks, bonds and real estate), and instead sought out alternative assets, which can continue to thrive in more difficult environments.

Pink diamonds were obviously one such asset, with prices continuing their steady performance all of last year, helped by the continued focus that this asset class has generated since the closure of the Argyle mine in late 2020.

With prices up more than 50% in the last two years, they are one of the few assets that have prospered throughout the entire COVID era and its aftermath, with strong supply/demand fundamentals set to support pink diamond prices, in 2023 and beyond.

Interest rates continue to climb

The Reserve Bank of Australia (RBA) met for the first time earlier this week, and as most analysts expected, they raised interest rates by 0.25%.

The increase, which marks the ninth meeting in a row that they’ve increased rates, with the official cash rate now sitting at 3.35%.

They likely have a way to go too, with the RBA at pains to point out that higher rates will likely be required to contain inflation rates which continue to surprise to the upside.

Indeed, some commentators now think that the RBA will continue to hike for most of the year, with the cash rate likely to climb beyond 4% before peaking, which will only exacerbate the pain felt by a lot of mortgage holders sitting on large debt piles.

This pain is beginning to show up in both soft and hard economic data, with retail sales now falling, while consumer confidence in Australia is plunging.

It’s also worth noting that given current inflation levels, even if the RBA does hike rates to 4%, the ‘real’ return (i.e. the rate one earns after inflation) on cash is likely to remain negative, for the foreseeable future at least.

This should help be bullish for investment demand for alternative assets, especially with home prices falling, and the share-market struggling.

Pink diamonds are set to be a particular beneficiary of this trend, as indeed they have been for some time, given their extremely limited supply, their strong performance track record, and their inflation hedging qualities, with all of these factors regularly coming up in the conversations that the team at Australian Diamond Portfolio have with our wonderful client base on an ongoing basis.

As always, we hope you’ve enjoyed this week’s edition of “In the Loupe” and we look forward to any questions or comments you may have.

Botswana’s President Mokgweetsi Masisi warned Sunday that his country could sever ties with South African diamond giant De Beers if talks to renegotiate a sales agreement prove unfavorable for his country.

The 2011 sales agreement governing the terms of marketing diamonds produced by Debswana – a 50-50 joint venture between the government and De Beers – expired in 2021.

It has been extended by the parties, who cited the coronavirus outbreak as the reason for the delay in concluding negotiations, and will end on June 30, 2023.

Speaking at a rally of his ruling Botswana Democratic Party (BDP) in his home village of Moshupa, about 65 kilometers from the capital Gaborone, Masisi warned, “If we don’t reach a win-win situation, each side will have to pack up and go home.”

Under the 2011 agreement, the mining company De Beers received 90% of the rough diamonds produced while Botswana, Africa’s largest diamond producer, received 10%. In 2020, Botswana’s share was increased to 25%.

In 2020, Botswana’s share was increased to 25%.

Today, “we got a glimpse of how the diamond market works, and we found out that we received less than we should have,” said Mr. Masisi, who spoke in both English and the local language, Tswana.

“We also found out that our diamonds are bringing in a lot of profit and that the (2011) agreement had not been favorable to us,” he added, before warning: “We want a bigger share of our diamonds. Business cannot continue as before.

Angola is aiming for a dual listing for state-owned diamond miner Endiama, reported Reuters citing Angola Mines Minister.

The country initially plans an initial public offering for a stake between 5% and 10% in the company on the Angolan stock exchange, following which it will seek a secondary foreign listing.

This move forms part of the OPEC member country’s efforts to reform and privatise the economy, including a partial listing of national oil company Sonangol.

Russian diamond mining company Alrosa has a joint venture with Endiama in Angola.

Following Russia’s invasion of Ukraine last year, sanctions were imposed by Western nations on several companies, including Alrosa, subsequently impacting Endiama’s operations.

Angola Minister of Mineral Resources, Oil and Gas Diamantino Azevedo told the news agency on the sidelines of a mining conference in Cape Town: “Sanctions are there and there is some impact.”

Azevedo said the government is considering measures required to avoid impacts on diamond production.

The minister noted that the government, however, could go ahead with an initial public offering for Endiama following its restructuring.

Azevedo said: “Our goal is (to list) till 30% but will start maybe with five or 10%.”

According to Endiama’s document at the mining conference, the firm’s production was about 8.75 million carats for 2022.

Between 2022 and 2027, Endiama intends to more than double its diamond production to 17.5 million carats.

In September 2022, Bloomberg News reported that Angola was looking to sell its 30% stake in Sonangol within the next five years.

Martin Rapaport recently released an incendiary memo to the diamond and jewelry industry calling on them to stop doing business in lab-grown diamonds (LGD), which he characterized as “synthetic” and “fraudulent.”

He also claimed those selling LGD were “operating dishonestly and unethically” and trading short-term opportunities at the expense of those that are “certain and sustainable.”

Rapaport is the ultimate industry insider, and there’s no question about which side his bread is buttered on. As chairman of The Rapaport Group, his company is a portal for information about and services to the diamond industry, including the Rapaport Price List, which it claims is the industry’s primary source for diamond price and market information, and an online diamond trading network, RapNet.

In a request for comment, a Rapaport representative shared the memo but added no additional comment.

Rapaport wrote:

“The greatest challenge facing the diamond trade is greed. Our trade is willfully destroying the underlying value of diamonds as a store of value through the marketing, promotion and sale of synthetic diamonds as a replacement for natural diamonds”

And he added, “Essentially, the diamond industry is trading short-term, unsustainable profits for the reputation of diamonds as a store of value.”

Then he went further, “Many – if not most – in our trade are operating dishonestly and unethically by failing to make full disclosure about the value retention of synthetic diamonds.”

And his memo concluded, “The Rapaport Group does not facilitate the sale of synthetic diamonds in any way. We believe they are a fraudulent product because of how they are sold. They are also a threat to the fundamental message of diamonds.”

This memo followed a submission to the Responsible Jewellery Council (RJC) in December 2021, where he pointed to Zales, James Allen, Jared, Diamond Direct (all Signet brands) and Brilliant Earth as not providing full disclosure about the LGD jewelry they sell. “Consumer expectations are not being managed honestly by unethical retailers,” he claimed.

According to lawyer Milton Springut, partner at Moses Singer, Rapaport’s disparaging and potentially injurious claims against lab-grown diamonds and the parties who do business in them probably don’t violate federal or state liability laws.

But Rapaport’s words are ill-chosen, and his claims are without merit, according to experts I spoke with.

Synthesized But No Less Real Lab-grown diamonds may be synthetic, as in made by man, but they are just as “real” as a natural diamond, as defined by the FTC. A diamond, no matter its origin is “a mineral consisting essentially of pure carbon crystallized in the isometric system. It is found in many colors. Its hardness is 10; its specific gravity is approximately 3.52; and it has a refractive index of 2.42.”

While lab-growns that meet the above criteria can be labeled as a “diamond,” the FTC also ruled that their man-made origin must be clearly disclosed.

So it requires marketers must precede the word “diamond” with “equal conspicuousness” such words as “‘laboratory-grown,’ ‘laboratory-created,’ ‘[manufacturer name]-created,’ or some other word or phrase of like meaning, so as to disclose clearly the nature of the product and the fact it is not a mined gemstone.”

It took a little while for some involved to find their footing under the new FTC guidelines, but now it seems all companies and retailers trading in lab growns have gotten on board and clearly, responsibly and honestly disclose the man-made, laboratory-grown origins of their stones.

That’s why Rapaport’s word choice of “synthetic” is over the line, implying that lab-grown diamonds are “simulants,” on the order of CZs or moissanite that may have a diamond-look, but are distinctly different in their physical properties and chemical composition.

“It’s an intentionally pejorative term because he is desperately trying to hold on to the tradition of mined diamonds,” said Marty Hurwitz, founder of market-research firm MVI Marketing LLC (THE MVEye) that specializes in the gem, jewelry and watch industries since 1987.

“One could argue using the term ‘synthetic’ may cause harm to lab-grown businesses, but it is clear that people who use the word are using it in a denigrating fashion,” he continued.

Hurwitz also notes the Gemological Institute of America (GIA), a non-profit educational and research organization that is the industry’s primary source for grading stones, doesn’t use the term “synthetic” any longer. It provided a limited grading program for lab-grown diamonds since 2007, then expanded and elevated it in 2020 as LGDs gained more industry and consumer acceptance.

GIA’s chief executive Susan Jacques described its decision as the natural evolution of the diamond market.

“We are responding to consumer demand,” she stated. “We want to make sure that consumers are educated, that we can protect their trust in the gem and jewelry industry as well as the products they are buying. As consumers adopt this new category, it’s important that we evolve with the new consumer.”

Value Is In The Meaning Rapaport’s rage against lab-grown diamonds seems to hinge on the fact that having an equivalent competing product in the market is causing the price of mined diamonds to fall. That’s the natural economic law of supply and demand.

And given that the prices of lab-grown diamonds are steadily falling, it is putting downward pricing pressure on mined diamonds too, reports diamond industry analyst Edahn Golan, though mined diamonds are experiencing a more moderate decline.

Then Rapaport goes one step further to claim that a mined diamond is a repository or “store of value” and that retaining, even increasing, its monetary value over time is part of the promise with purchase. This is patently false, both Hurwitz and Golan affirm.

“There is limited to no investment value in diamonds,” Hurwitz said. “Some categories of mined diamonds are investment grade and go up in value, but most diamonds depreciate faster than a car leaving the showroom. The average consumer has been fed a marketing myth, the greatest marketing story ever told. Most consumers never find out the truth because they don’t resell their diamonds.”

Golan added that jewelers have perpetuated the myth by offering a trade-in, so a purchaser of a $2,000 diamond ring can get that back in credit if they return to purchase a bigger, more expensive stone.

“I’m hearing the big trend in America now is for people who want to upgrade their engagement ring decide to keep their original stone and have it made into something else, like a pendant,” he said.

People hold onto their stone because of its sentimental, symbolic value, which is where the actual value lies, as Warren Buffett said, “Price is what you pay. Value is what you get.”

DeBeers tried to equate the two with its rule that a man should pay two-to-three months’ salary on an engagement ring. But ironically, that’s turned back on the industry because, with a lab grown, he can buy a bigger, more impressive stone that speaks even louder of his love for her when he pops the question.

Nothing Unethical, Fraudulent Or Dishonest Selling Lab Growns Rapaport goes too far when he suggests that there is something unethical, fraudulent or dishonest in selling lab-grown diamonds.

“The idea that diamonds are a store of value is a fundamental component of diamond demand. Consumers are being misled by retailers who sell man-made diamonds without full disclosure. The default assumption among consumers is that man-made diamonds will appreciate over time, even though the opposite is true,” he stated in his RJC filing.

One could argue that what is unethical, fraudulent and dishonest is suggesting that a mined diamond retains, even grows in monetary value.

“Rapaport is thinking like a diamond trader. Trading prices move up and down with the market. When they go up, it’s good; when they go down, it’s bad,” Golan said, noting that the increasing availability and consumer demand for lab growns is moving the needle for mined diamonds in the wrong direction.

Unlike traders, retailers think about cash flow, margins and turns. And this is where lab-grown diamonds have the edge.

“Jewelry stores hold loose diamonds on hand and the margins on loose natural diamonds is around 36%, while the margin for LGD was 54% at the end of December. And if it takes a retailer a year to sell a mined stone, but it only averages seven months to sell a lab-grown, a retailer will make more money at the end of the year,” Golan explained.

Hurwitz rhetorically asks, “Should we tell the consumers who are walking into our stores asking for lab-growns to go away? Should we say, ‘We don’t want to sell you this product that means incredibly high margins and profits for us and incredibly high value to you?’”

Retailers that trade in lab-growns are transparent and honest about the origin of their stones. The FTC requires it. There is nothing unethical, fraudulent or dishonest for a retailer to sell a customer what they want at the price they want to pay and to make money in the process.

“Half the diamonds are sold in the United States, and 50% of the business in the United States is bridal. The natural diamond industry is losing a chunk of that ‘Holy Grail’ to lab growns. The industry has to adapt to the changing world. It’s a combination of a cultural and business change that are driving each other,” Golan shared.

Can’t Turn Back The Clock “Rapaport has a tremendous self-interest in seeing the mined diamond business continue to thrive,” observed Hurwitz. “He’s trying to ensure that things never change. He wants to hold onto the tradition, but that’s futile.”

While Rapaport may be trying to valiantly to save the mined diamond industry, he may be doing more harm than good.

“The good news for the lab-grown diamond industry is that he appears to be going off the rails in his attacks, and as a result, fewer and fewer people are listening to him,” Hurwitz said.

“There is a consumer revolution happening because of lab-grown diamonds. As an industry, we must embrace the change and give consumers a choice.” he continued.

“Rapaport just wants to tell everybody that this product is good and that is bad. But the only voice that matters is the consumer. And the consumer is organically and very virally embracing this new product.”